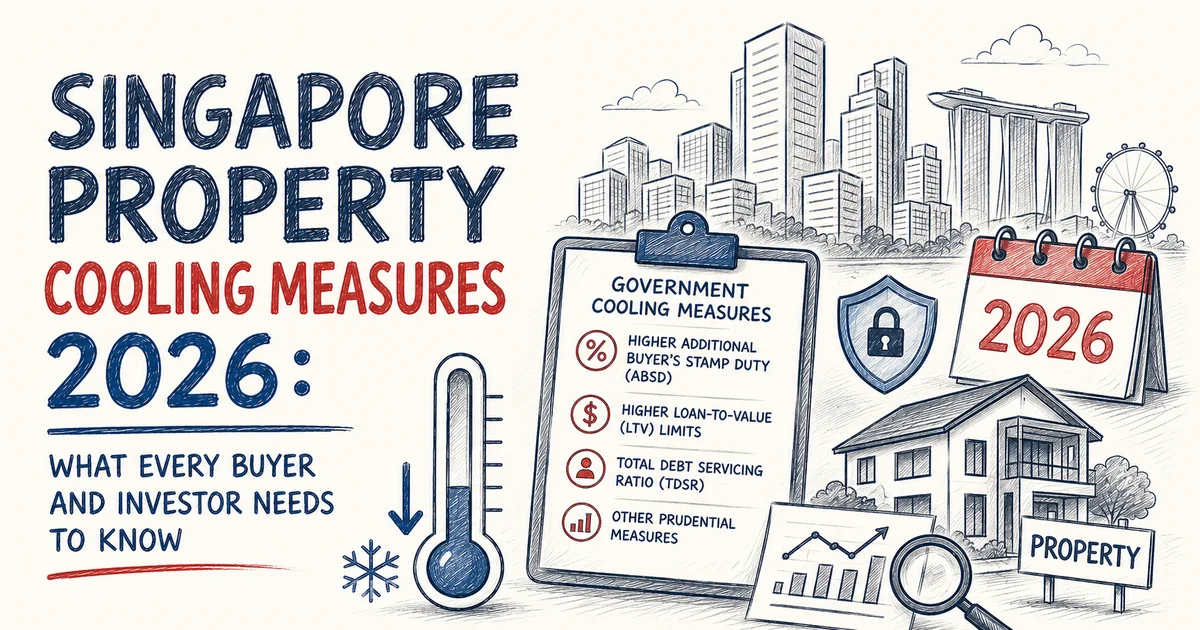

As of mid-2026, all five of Singapore’s main property cooling measures, ABSD, LTV, TDSR, MSR and SSD remain fully in force, with no sign of easing. Rather than waiting for a policy change that may not come, the smarter move is to understand the rules as they stand today and plan around them. Here’s a plain-English breakdown of each measure and what it means for your next purchase.

If you’ve been sitting on the fence about buying your next property, whether upgrading from your HDB flat or adding to an investment portfolio, you’ve probably heard someone say “wait for the cooling measures to ease.” I get this question almost every week, and the honest answer is that neither MND, MAS nor HDB has signalled any plan to relax the current rules.

What Are Cooling Measures, and Why Do They Exist?

Cooling measures are policy tools the government uses to keep Singapore’s property market stable and prevent excessive speculation. They’ve been introduced and adjusted in rounds since 2009, with the most recent significant tightening in April 2023 and further adjustments through 2025. The goal isn’t to punish genuine homebuyers, it’s to discourage over-leveraging and speculative flipping, which is why owner-occupiers generally face lighter restrictions than investors and multiple-property owners.

Additional Buyer’s Stamp Duty (ABSD): The Big One

ABSD is usually the single largest cost for anyone buying a second property or beyond. These rates have applied since 27 April 2023:

| Buyer Profile | 1st Property | 2nd Property | 3rd & Subsequent |

|---|---|---|---|

| Singapore Citizen | 0% | 20% | 30% |

| Singapore PR | 5% | 30% | 35% |

| Foreigner | 60% | 60% | 60% |

| Entity (company) | 65% | 65% | 65% |

For a $1.5 million condo, a Singapore Citizen buying a second property pays $300,000 in ABSD alone, on top of the usual Buyer’s Stamp Duty. This is exactly why strategies like timing your purchase around your MOP, or ABSD-free alternatives such as commercial property have become so common. For the full strategic picture, read my guide on Understanding ABSD for Property Investors.

Loan-to-Value (LTV): How Much the Bank Will Lend

LTV caps how much you can borrow relative to the property’s value or price, whichever is lower:

| Housing Loan | Maximum LTV | Minimum Cash + CPF |

|---|---|---|

| 1st housing loan | 75% | 25% |

| 2nd housing loan | 45% | 55% |

| 3rd or subsequent | 35% | 65% |

HDB concessionary loans now also cap at 75% LTV, reduced from 80% on 20 August 2024 to align with bank loans. The practical impact is big: a $1.5 million second property at 45% LTV means funding $825,000 upfront through cash and CPF, before stamp duties. This is a common blind spot for HDB upgraders who assume the next purchase will feel like the first. (Note: LTV limits are further reduced if the loan tenure exceeds 30 years or extends beyond the borrower’s age of 65.)

TDSR and MSR: The Ratios That Decide Your Loan Quantum

Total Debt Servicing Ratio (TDSR)

TDSR caps all your monthly debt obligations, property loans, car loans, credit-card minimums, personal loans at 55% of gross monthly income. It applies to any bank loan for private property or HDB flats.

Mortgage Servicing Ratio (MSR)

MSR applies specifically to HDB flats and Executive Condominiums, capping the housing loan repayment alone at 30% of gross monthly income. It’s stricter than TDSR and is often the binding constraint for HDB upgraders still financing their current flat.

Before viewing units, get an in-principle approval (IPA) from a bank so you know your real loan quantum — not just what you hope to borrow.

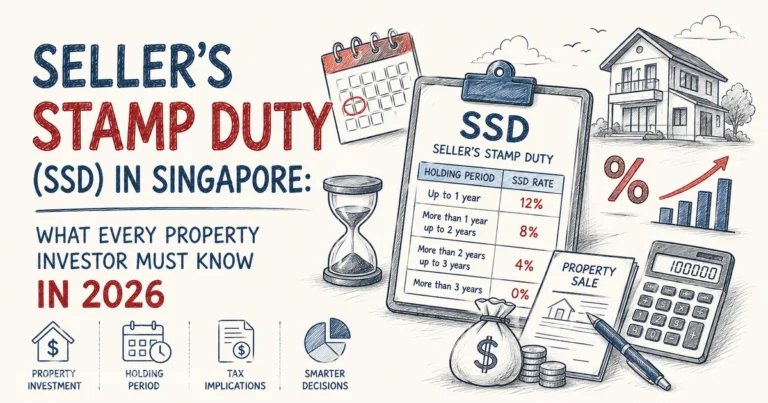

Seller’s Stamp Duty (SSD): The Short-Term Seller’s Trap

SSD was tightened from 4 July 2025, the holding period rose from 3 to 4 years, and each tier increased by 4 percentage points:

| Property Sold Within | SSD Rate |

|---|---|

| 1 year | 16% |

| 2 years | 12% |

| 3 years | 8% |

| 4 years | 4% |

| More than 4 years | 0% |

If you’re an investor eyeing a quick flip, or an upgrader who might need to sell a new private property sooner than planned, this 4-year window needs to be front and centre. Selling even a few months early can cost tens of thousands of dollars. (HDB flats are generally unaffected because the 5-year MOP already exceeds the SSD window.)

How to Plan Around the Rules, Not Against Them

- Time your ABSD exposure. If upgrading, consider selling your existing property first, or for married couples buying jointly within 6 months of the new purchase to qualify for ABSD remission. Our HDB upgrader timeline guide maps out the full sequence.

- Stress-test your TDSR/MSR first. Know your borrowing ceiling, then shop within it.

- Budget for the full LTV gap. For second properties, make sure your cash and CPF can cover the 55% you won’t be borrowing.

- Think in 4-year horizons. If there’s any chance you’ll sell within 4 years, price in the SSD.

- Explore legitimate ABSD-free structures such as commercial property if you’re purely investing and have exhausted your residential ABSD headroom.

Key Takeaways

- All five cooling measures remain in force in 2026, plan around them rather than waiting for them to ease.

- ABSD is the biggest cost: 20% for a Singapore Citizen’s second property, 30% for a third.

- LTV on a second loan is just 45% (75% on your first), the upfront cash/CPF gap is large.

- TDSR (55%) applies to all loans; MSR (30%) adds a stricter cap for HDB and EC.

- SSD now runs 4 years (since July 2025) at 16/12/8/4%, hold longer, or budget for it.

Frequently Asked Questions

Are Singapore’s property cooling measures being relaxed in 2026?

No. As of mid-2026 there is no indication that the government intends to ease ABSD, LTV, TDSR, MSR or SSD. The most recent change was a tightening of Seller’s Stamp Duty in July 2025. Buyers should plan around the current rules rather than wait for them to loosen.

What is the ABSD rate for a second property in Singapore?

A Singapore Citizen pays 20% ABSD on a second residential property and 30% on a third. Permanent Residents pay 30% and 35% respectively, foreigners pay a flat 60%, and entities pay 65%. These rates have applied since 27 April 2023.

How much can I borrow for a second property?

Your second housing loan is capped at 45% LTV, so you must fund at least 55% of the price through cash and CPF, with a minimum of 25% in cash. A third or subsequent loan is capped at 35% LTV.

What is the difference between TDSR and MSR?

TDSR caps your total monthly debt repayments at 55% of gross income and applies to all property loans. MSR is stricter and applies only to HDB flats and Executive Condominiums, capping the housing loan repayment alone at 30% of gross income.

How long must I hold a property to avoid Seller’s Stamp Duty?

Since 4 July 2025, you must hold a residential property for more than 4 years to avoid SSD. Selling within 1, 2, 3 or 4 years incurs 16%, 12%, 8% or 4% respectively. HDB flats are generally unaffected because the 5-year MOP already exceeds this window.

Get Your Numbers Before You Commit

Cooling measures aren’t going anywhere in 2026 — but they’re not a reason to put your plans on hold indefinitely. With the right structuring and timing, both HDB upgraders and investors can still move forward confidently. The key is personalised numbers, not generic rules of thumb.

For a clear, no-obligation breakdown of exactly how ABSD, LTV and TDSR/MSR apply to your situation, contact Shawn Sum at +65 9239 4968 or visit shawnpropertyhub.com. You can also request a free indicative valuation to begin.

Disclaimer: This article is for general information only and is not financial, legal or tax advice. Cooling-measure rates and policies are subject to change by the Singapore government. Please verify current rates with IRAS, MAS and HDB, and consult a qualified financial adviser or conveyancing lawyer before making any property decisions.