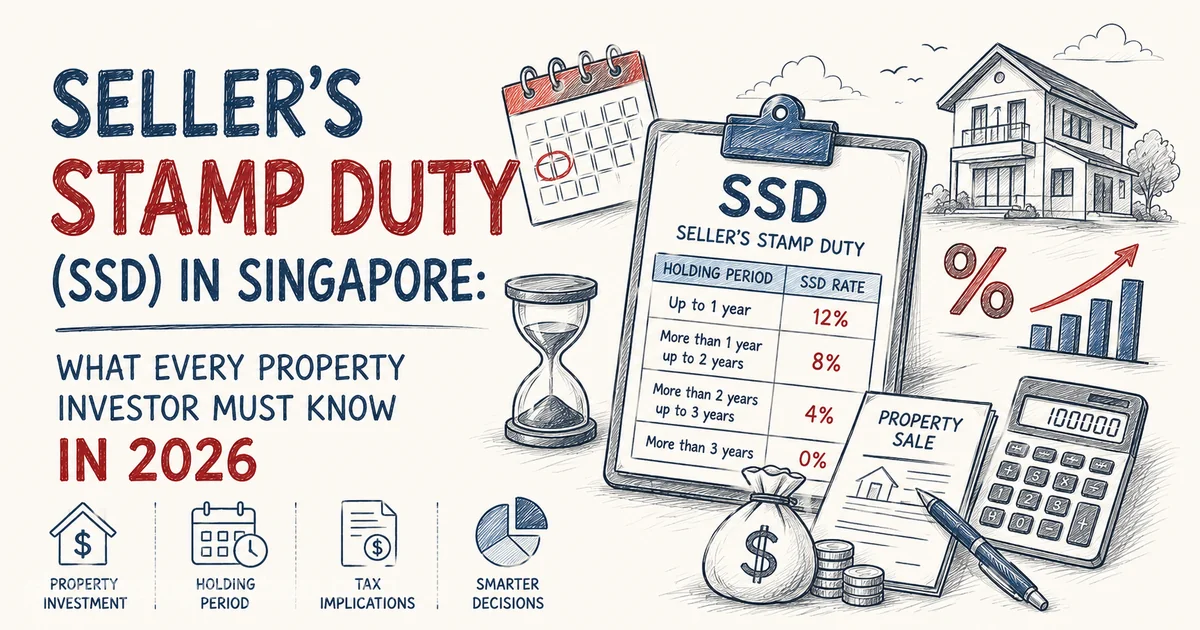

Seller’s Stamp Duty (SSD) is a tax on any residential property you sell within a set holding period after buying it, designed to discourage short-term flipping. For homes bought on or after 4 July 2025, that period is 4 years, with rates from 16% (sold within 1 year) down to 0% after 4 years. It is charged on the higher of the sale price or market value, and it is completely separate from ABSD, which you pay when you buy.

Most investors obsess over the costs of buying ABSD, loan quantum, legal fees. But there is a tax that catches people out on the way out, and in 2025 it got a lot sharper. Get it wrong and you could hand over tens of thousands of dollars unnecessarily. Get it right and you build your exit strategy around it from day one.

What Is Seller’s Stamp Duty?

SSD is a tax you pay when you sell a residential property within a certain number of years of buying it. It was introduced as a cooling measure to discourage short-term speculation, the “buy cheap, flip fast” behaviour that inflates prices and destabilises the market.

The key principle: the shorter you hold the property before selling, the higher the SSD rate. Hold it long enough and SSD drops to zero. Crucially, SSD is separate from ABSD, ABSD hits you when you buy, SSD hits you when you sell early. A savvy investor plans for both; for the full picture of how these fit together, see our guide to Singapore’s property cooling measures.

The Big 2025 Change Investors Can’t Ignore

On 3 July 2025, the Government announced significant changes that took effect for all residential properties purchased on or after 4 July 2025, with no transition period:

- The holding period was extended from 3 years to 4 years.

- The SSD rates were raised by 4 percentage points for each tier.

So the rules now depend on when you bought.

Properties purchased on or after 4 July 2025 (current rules)

| Property Sold Within | SSD Rate |

|---|---|

| 1 year | 16% |

| 2 years | 12% |

| 3 years | 8% |

| 4 years | 4% |

| More than 4 years | 0% |

Properties purchased 11 March 2017 – 3 July 2025 (older rules)

| Property Sold Within | SSD Rate |

|---|---|

| 1 year | 12% |

| 2 years | 8% |

| 3 years | 4% |

| More than 3 years | 0% |

These revised rates effectively bring SSD back to pre-2017 levels, a clear signal the government wants to curb quick flips. One detail sellers often miss: the holding period is counted from the date you accept the Option to Purchase (OTP), or the date the Sale and Purchase (S&P) Agreement is signed — not from the completion date or key collection.

What SSD Actually Costs You: A Worked Example

Say you bought a $1.5 million condo in August 2025 (so the new rules apply) and circumstances force you to sell 18 months later that falls within Year 2, so the SSD rate is 12%.

12% of $1.5 million = $180,000 in SSD.

That is not a typo. On a property that may have appreciated only modestly, a $180,000 tax bill can easily turn a paper gain into a real loss once you also account for agent fees, legal costs and interest paid. Compare that to selling just after the 4-year mark: SSD would be $0. The difference between selling in month 18 versus month 49 could be $180,000 in your pocket for the exact same property. This is why I tell every investor the same thing: decide your minimum holding period before you buy, not after.

How Smart Investors Plan Around SSD

You don’t beat SSD with clever tricks, you beat it with disciplined planning.

Build a minimum 4-year horizon into your strategy

If you’re buying under the current rules, treat 4 years as the earliest realistic exit. Anything sooner should only be a genuine emergency, with the SSD cost consciously accepted.

Stress-test your holding power

Before buying, ask: can I comfortably service this mortgage for at least four years, even if rental income dips or interest rates rise? If the honest answer is shaky, you’re exposed to a forced, SSD-triggering sale. Cash buffers matter more than ever.

Factor SSD into your ROI from the start

When you model returns, run a scenario where you’re forced to exit early. If the deal only works assuming a quick flip, it’s probably too fragile for today’s environment.

Know the exemptions

SSD doesn’t apply in every situation. Licensed housing developers are exempt on properties they develop, and public authorities such as HDB and JTC are exempt when carrying out their functions. There are also specific relief scenarios, always check the latest IRAS guidance for your circumstances rather than assuming.

Time your entry and exit deliberately

Because the clock starts at OTP acceptance, keep clear records of your purchase date and count forward carefully. Selling even a few weeks past a tier boundary can save you a full percentage tier of tax.

Where SSD Fits in the Bigger Picture

SSD works alongside ABSD, TDSR and the LTV limits as part of Singapore’s broader toolkit to keep the market stable. For investors, the takeaway is that the era of quick flips is firmly over, the system is deliberately designed to reward patient, long-term holders who buy quality assets, hold through cycles, and let genuine appreciation and rental yield do the work.

In my experience, the investors who consistently build wealth in Singapore property aren’t the ones chasing fast exits, they’re the ones with the holding power and patience to ride out the SSD window and beyond. If you’re also weighing an upgrade rather than a pure investment, our HDB upgrader timeline guide maps out the sequence.

Key Takeaways

- SSD is charged when you sell a residential property within the holding period, on the higher of sale price or market value.

- For properties bought on or after 4 July 2025: a 4-year holding period, rates of 16% / 12% / 8% / 4%, then 0%.

- For properties bought 11 Mar 2017 – 3 Jul 2025: a 3-year holding period, rates of 12% / 8% / 4%, then 0%.

- The holding clock starts at OTP acceptance, not completion.

- Plan a minimum 4-year hold and stress-test your finances before you buy.

Frequently Asked Questions

What is Seller’s Stamp Duty (SSD) in Singapore?

SSD is a tax payable when you sell a residential property within a set holding period after purchase. It was introduced as a cooling measure to discourage short-term property flipping. The shorter you hold before selling, the higher the rate; hold beyond the holding period and no SSD is payable.

What are the current SSD rates in 2026?

For residential properties bought on or after 4 July 2025, SSD is 16% if sold within 1 year, 12% within 2 years, 8% within 3 years, 4% within 4 years, and 0% after more than 4 years. Properties bought between 11 March 2017 and 3 July 2025 follow the older rates (12% / 8% / 4% over a 3-year period).

How long must I hold a property to avoid SSD?

For properties bought on or after 4 July 2025, you must hold for more than 4 years to pay no SSD. For properties bought before that (from 11 March 2017), the holding period is more than 3 years.

When does the SSD holding period start?

It starts from the date you accept the Option to Purchase (OTP) or Sale and Purchase Agreement is Signed, not from completion or key collection. Keep clear records of your acquisition date and count forward from there.

Who is exempt from Seller’s Stamp Duty?

Licensed housing developers are exempt on properties they develop, and public authorities such as HDB and JTC are exempt when carrying out their official functions. Certain relief scenarios also apply — verify your specific situation with IRAS.

Is SSD the same as ABSD?

No. ABSD (Additional Buyer’s Stamp Duty) is paid when you buy an additional property; SSD is paid when you sell a property too soon after buying it. They are separate taxes and an investor should plan for both.

Plan Your Exit Strategy Before You Buy

If you’re weighing an investment purchase in 2026, don’t let SSD blindside you. I’d be happy to map out your holding-period exposure, run the actual SSD figures against your goals, and help you structure a purchase that protects your returns — whether it’s your first investment condo or an expanding portfolio.

Reach out to Shawn Sum at +65 9239 4968 or visit shawnpropertyhub.com, or request a free indicative valuation to begin.

Disclaimer: This article is for general information only and is not financial, legal, tax or property advice. SSD rates, holding periods and exemptions are set by the Singapore authorities (IRAS, MAS, URA) and are subject to change. Figures are accurate as of July 2026 to the best of our knowledge. Always verify the latest rules with IRAS and seek independent professional advice before any property or tax decision.